Kevin Warsh Comes to Town But the Donald Ain’t Gonna Like What Happens Next

Here is a salient place to start regarding the economic impact of the Donald’s misbegotten war on Iran: To wit, approximately 7 billion ton-miles of freight moves by truck each and every day in the USA, which heavy truck fleet consumes upwards of 2.9 million barrels per day (mb/d) of diesel fuel.

Alas, the price of diesel fuel was about $3.55/gallon both a year ago and as of early January 2026, but has since soared by more than+$2.00 per gallon to $5.60. That’s a 56% rise in the cost of pumping goods and commodities through the arteries of the US economy. On an annualized basis, the diesel fuel bill for the US truck fleet went from $155 billion per year to $250 billion per year at current oil prices.

The big question, of course, is through which channel these drastically higher fuel acquisition costs will be absorbed—in higher prices or reduced output? And that pertains not just to the microcosm of the trucking sector, but the entire GDP now being battered by the Donald’s elective war-based dislocation of the world’s 175 million BOE/day oil and natural gas markets.

We’d bet it will be a combination of both inflation and deflation, otherwise known as stagflation. The mix of these outcomes depends upon supply and demand conditions in individual sectors of the economy in part, but also, and ultimately and more importantly, on the Fed. That is, whether the nation’s central bank pumps incremental demand into the economy via credit expansion with a view to “accommodating” the soaring price of energy today, and, soon, food and other commodity inputs to GDP, too; or holds firm on the printing press dials and allows the now cresting energy and commodity shocks to work their way through the interstices of the $30 trillion US economy.

Of course, during the previous comparable petroleum supply disruption during the 1970s, the Fed made the huge mistake of printing the money to counteract what was a “supply shock” in the form of soaring petroleum prices. But that led—just as sound money advocates had always held—to double digit increases in the general price level by the end of the decade, and thereafter the trauma of the Volcker administered application of the monetary brakes.

With the Fed fixing to welcome a new Chairman, as today’s congressional hearings remind, it is therefore a question of whether or not the Kevin Warsh Fed will want to take its place in the monetary policy villains gallery along with Arthur Burns and the hapless William G. Miller.

We think not. We actually believe that for the first time since Volcker we are about to get a Fed chairman who understands the requisites of sound money and noninflationary finance, as well as the profound error of Keynesian demand management at the central bank.

And not only that. As far as we can tell, he also has the experience from his prior service on the Fed during the so-called Great Financial Crisis and the cajones to lean heavily against the supply shock now emanating from the Persian Gulf.

Of course, in a perfect world of honest money and free markets—including in the production of money and credit—there wouldn’t be any central bank “leaning” to do. Under an honest money gold standard, for instance, the impending petroleum supply shock would cause relative price changes, thereby generating a sharp curtailment of activity in petroleum intensive sectors and the reallocation of activity, output, jobs and capital to less petroleum intensive sectors. That’s what the miracle of free markets do when they are allowed by the state to operate.

We obviously do not have anything close to free money and capital markets today. Yet we may be lucking out with the arrival of a new Fed Chairman who might well attempt to stand up a sound money proxy—at least in part—to simulate the deflationary and re-allocative impulses that would otherwise arise in the face of a world scale supply shock. That is to say, Warsh may well allow the incoming Persian Gulf supply shock to curtail output in heavily impacted sectors rather than monetize it, as did his failed predecessors during the 1970s.

Moreover, one thing which may well help Walsh lean in this anti-Keynesian direction is the the need to avoid the tattered legacy of the private equity based deal lawyer who proceeded him. As it happened, Powell had no clue that the blue suits who soon sourrounded him at the Eccles Building were wrong-headed Keynesian monetary statists through and though.

Accordingly, when the far smaller supply shock from the Black Sea dislocation at the on-set of the Russia-Ukraine War came cascading through the global energy and food commodity markets, Powell joined the Burns/Miller brigade and kept on accommodating.

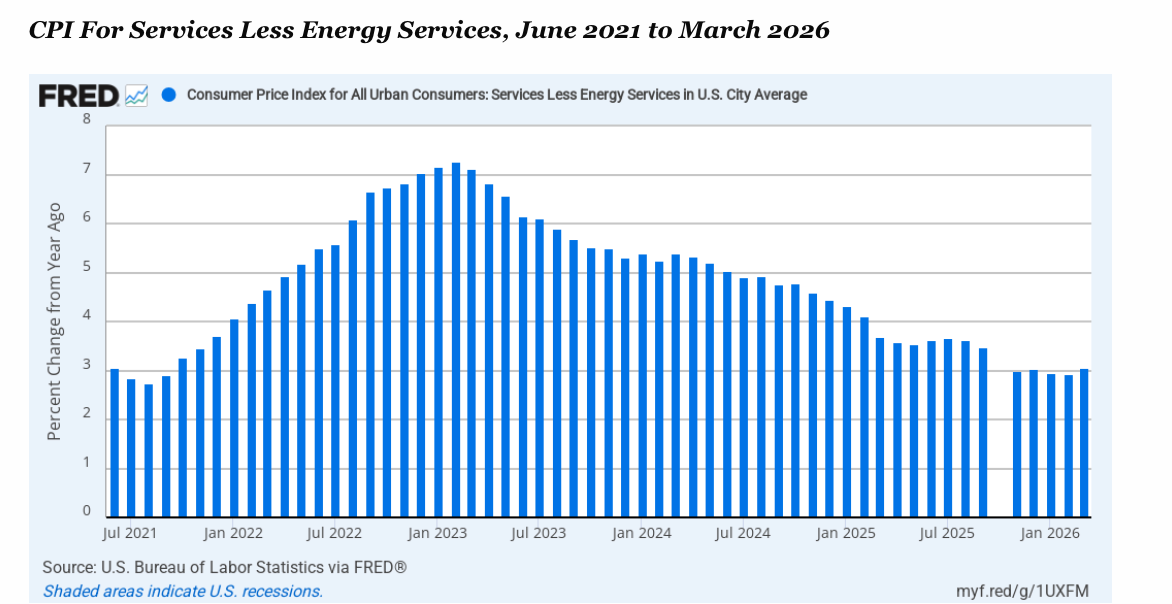

That’s evident in the graph below, which depicts the domestic services inflation rate excluding energy. This is the Fed’s go to inflation metric because it arguably measures a subset of prices in the US economy that are mainly driven by so-called domestic “demand”, which is the very thing the Fed claims to be expert at calibrating.

We think Fed “demand management” is pretty much mischievous nonsense. The fact is, however, when the Ukraine War incepted in February 2022 the domestic services less energy index was already rising at a 4.1% Y/Y rate. So there was no room for “accommodation” at all.

In fact, the Ukraine War supply shock had caught the Fed with its monetary pants down. The Fed funds rate was effectively zero in nominal terms at the time (February 2022) and had been pinned to the zero bound for the previous 22 months. Thereafter Powell and his merry band of money printers kept kidding themselves into believing that the Ukrainian War inflation surge was “transitory” and that a Volcker style slamming of the monetary brakes was unnecessary.

As it evident in the chart, however, the Fed tepid 25 basis points increases month after month in its target Fed funds rate was blatantly too little and way too late. By February 2023, the very inflation metric that the Keynesian central bankers claim to heavily influence—-domestic services less energy services—was leaping higher at a +7.3% Y/Y rate.

By then, of course, and with double digit energy and food inflation layered on top, headline inflation was running at 40-year highs and knocking on the door of 1970s style double digit inflation.

We think this history is profoundly relevant to where a Kevin Warsh-led Fed may come out because it just so happens that the the Y/Y rate on this key metric stood at +3.05% in March 2026 or about where it had been in October 2021 on the eve of the “Powell Inflation”.

We don’t think Kevin Warsh, who is a real student of money and economics, wishes to be placed next in line in the Burns/Miller/Powell gallery of monetary villains.

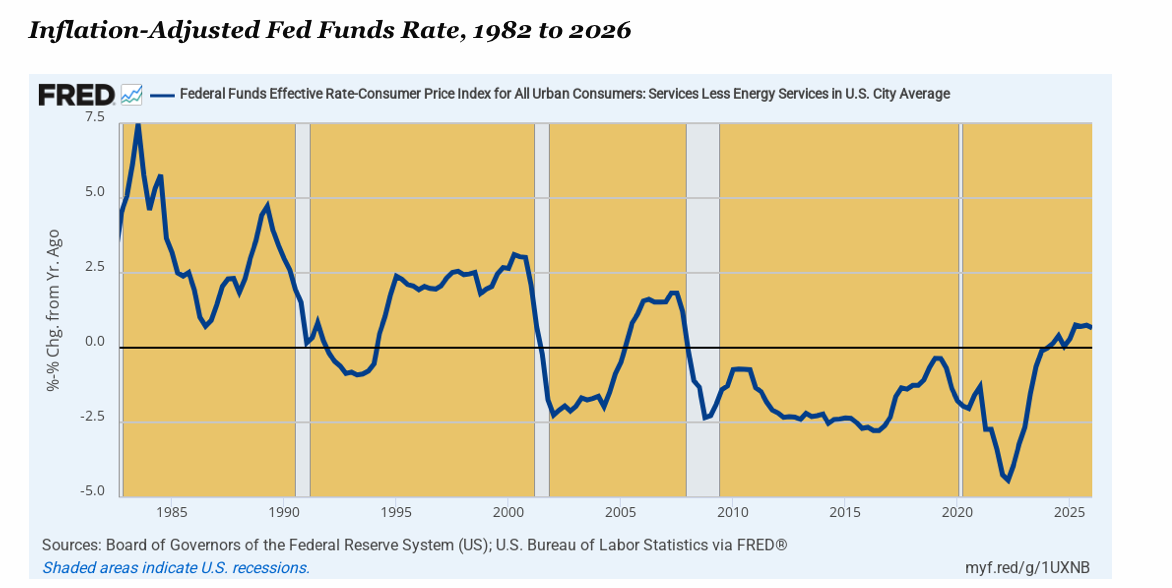

That especially the case when you look at the history of the Fed’s so-called monetary target adjusted for the prevailing (Y/Y) inflation rate. To wit, there is no logical or sustainable world in which the inflation-adjusted or “real” cost of overnight money can be negative for any even limited period of time.

That’s because negative cost overnight money in real terms is truly the mother’s milk of speculation—especially on Wall Street among the hedge funds and fast money operators, but on the main street economy, too. Stated differently, cheap money everywhere and always causes excessive speculation, imprudent leverage, debt accumulation, financial asset bubbles, capital malinvestment and economic waste. But above all else it also fuels an inflationary rise in the general price level owing to artificial credit-fueled demand uncoupled from any prior and corresponding increase in supply.

In this context, the chart below tells you all you need to know about what the Warsh Fed will be up against, and also the lessons of the 2022-2023 error by the Fed in its delayed and languid reaction to the Black Sea commodity shock. To wit, the inflation-adjusted Fed funds rate in Q2 2022 when measured by the inflation metric the Fed swears by—the domestic services CPI less energy services—-was negative -4.4%.

Surely that was a signal that the money-printers were way over the end of their skis. That’s especially because the Fed funds rate had been negative in real terms for 57 quarters running, going all the way back to Q1 2008, when the real funds rate had last been slightly positive.

But here’s where the inflationary gale force was gestated. It actually took the Fed more than three years—until Q2 2025—-to get the Fed funds rate positive in real terms, and then only marginally so at just +0.75%. Indeed, it is nothing less than the big pool of negative real cost money printed by the Fed during those three years that rocked the US economy with an inflationary outbreak that is still not fully extinguished.

In fact, as the US economy now begins to absorb the far more powerful supply shock waves emanating from the Persian Gulf, the real Fed funds rate was still only a scant +o.66% as of Q1 2026. In that circumstance, and given the near miss into runaway double digit inflation during the mid-2022 Black Sea supply shock, we think the incoming Warsh Fed is not about to run a repeat of 2021-2022.

The more likely course is actually suggested by the left-hand side of the graph, which shows that the real funds rate measured with this metric hovered in the +2.5% range or higher during the salad days of non-inflationary growth of the 1980s and 1990s. That is to say, Kevin Warsh is likely to prove to be more of a Volcker/Reagan sound money central banker than we have experienced since Alan Greenspan sold his gold standard bona fides for a stint as the world’s most famous money-printing after the dotcom crash.

So the question recurs. What is likely to happen to the alleged Trumpian Golden Age when the Persian Gulf Supply shock smacks up against the incoming sounder money Fed under Kevin Warsh?

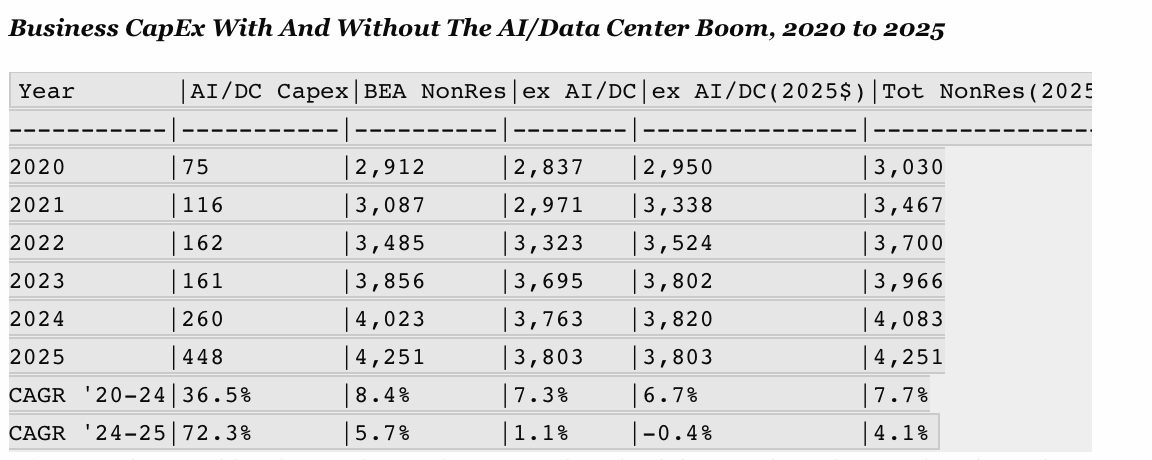

In a word, we think the US economy is already teetering on the edge of recession, waiting for the proverbial wing-flap to tip it over into contraction. After all, it’s already evident that the one bright spot in the US economy during the Donald’s second go round—capital spending—is purely an artifact of the stock market bubble in AI.

For want of doubt, the table below shows Capex spending for AI and data centers and compares it to the second column, which is the standard measure of business fixed investment in structures, equipment and intellectual capital as reported in the income and product accounts. It is notable that the former accounted for just 2.5% of business capital investment in 2020, but grew by $188 billion in 2025 versus prior year.

At the same time, total business investment rose by just $228 billion in 2025, meaning that the AI/data center boom accounted for fully 82% of total business investment spending growth in the US economy during 2025.

The final two columns show the same data in constant dollar terms. Whereas the reported data shows that real nonresidential fixed investment investment (fifth column) rose by a seemingly robust 4.1%during Trump’s first year, capital spending excluding the AI bubble actually shrank at a -0.4% annual rate.

As it happened, the latter had actually grown by 6.7% per annum during the time of Sleepy Joe (2024-2024) owing to the unsustainable stimulus of borrow, spend and print after the pandemic collapse in the spring of 2020.

So “Joe Biden” therefore gets no plaudits for the artificially bloated economy he inherited from Trump 45 and the money-printing excesses of the Powell Fed. Still, it can be well an truly said that the US economy was already positioned on a banana peel when the Donald elected to blow up the Persian Gulf for no good reason of homeland security.

Of course, the Donald makes up the numbers to suit has glandular impulses whenever he takes to his Truth Social soapbox. On that forum he has claimed, for instance, that the US is in the middle of a booming recovery of the manufacturing sector owing to his big beautiful tarrifs.

Alas, his victory on that front is about is vacuous as are his daily claims to having won the war against Iran. There is not a shred of truth to it, as the constant dollar level of manufacturing shipments depicted in the graph below clearly shows. To wit, real shipments have flat lined for years and stand 13% below their recent peak in Q4 2007.

In short, the Persian Gulf supply shock is about to monkey-hammer the US economy good and hard. And then the AI bubble in the stock market will bust—even as there will be no money-printers at the central bank waiting to bailout the mess.

So we welcome the impending arrival of Kevin Warsh at the Eccles Building—a man who at last may partially fill Paul Volcker’s big shoes. But we are quite sure that at the first opportunity, the Donald’s stubby little fingers will be pounding on the Truth Social keyboard about another “stupid” traitor who failed to do his bidding.

Welcome back to Trumpified Washington, Kevin!

https://davidstockman.substack.com/p/kevin-warsh-comes-to-town-but-the-630