Iran War Effect Marks the Resetting of World Geo-Politics

Seemingly, every day brings breathless new claims that an US-Iran ‘deal’ awaits only a signature. As so often happens, the mediators (Pakistanis and Qataris) hope to manage both sides by telling one side that the other party is at the brink of agreement when it is not so, especially in an atmosphere of total mistrust. By these means the mediators hope to push matters towards a final agreement. It is a familiar tactic, but one that quite often results in confusion and distrust — rather than the hoped-for settlement.

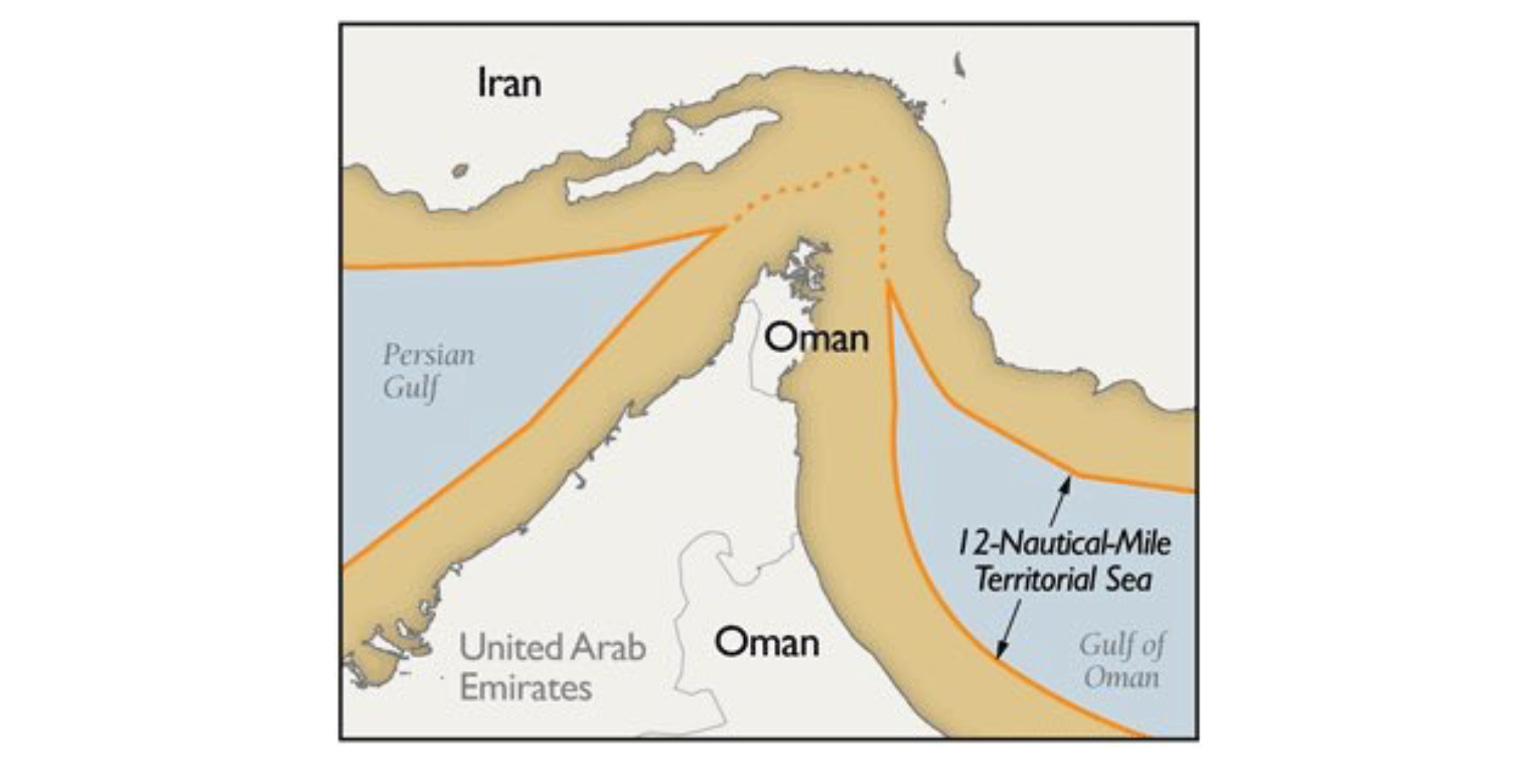

The ‘plan’ at this stage has only two central pillars: Iran’s ‘reopening’ of the Strait of Hormuz (on Iran’s terms) in return for the lifting of the US naval blockade, and — at a later date — an understanding that the dilution of Iran’s 60% enriched uranium would be tackled in return for an end to sanctions.

To say the devil is in the detail would be the understatement of the year. Iran understands that Trump’s headliners of an ‘imminent deal’ are firstly, intended to keep the US stock market up and oil futures trading well below that of the delivery price of physical oil. And secondly, to obfuscate that Trump may be seeking a plausible way to end the war via striking a quick, incomplete deal that would, in all likelihood, be largely on Iran’s terms.

All other issues — including the crucial detail of any nuclear agreement — would be deferred.

Trump wants from Iran an initial concession that he can hail as a visible win — and one that will please markets, too. But Iran will not trade its military leverage, and certainly not the strategic dominance that it achieved in the war, nor Hormuz, for fuzzy assurances from the mediators. Iran does not trust the US one iota.

Ali Akbar Velayati, Senior Adviser to Iran’s Supreme Leader observes,

“History bears witness that everyone who came seeking domination, from Alexander to Genghis Khan and Trump, ultimately ended up dissolving into the heart of ancient Iranian civilisation. This time, Iran’s red line is clear: papers and signatures alone are no guarantee. The tangible guarantor of the agreement’s survival is the Strait of Hormuz”.

“For geography does not lie. It is the final judge over every covenant written on paper”.

The mediators naturally are desperate to avoid another round of war. Iran however, demands hard detail. This is Trump’s dilemma. He wants a quick win, but the mere hint of a fudged, incomplete deal — mainly on Iran’s terms — brought the wrath of the pro-Israel billionaire class down upon his head (the pushback was intense), and Israel (likely with encouragement from that same class) then blew up Trump’s ceasefire by launching a scorched-earth military assault on Lebanon, and on Gaza and its citizens, so breaching the ceasefire precondition for any deal.

Trump is in zugzwang. (Any move he makes, potentially only worsens his position, whether strategically or domestically).

Territorial waters in the Strait of Hormuz (Source)

We saw this same zig-zagging, back of an envelope, non-strategy perfectly illustrated in the iconic imaging from Trump’s Beijing visit — Trump ‘winged it’; no prior preparation; a ‘seat of the pants’ summit.

That image may perhaps come to define this era — today’s iconic moment was of a US President wearing the air of defeat whilst a confident President Xi’s comportment demonstrated who was in control.

Why, one may ask, would the pro-Israel class risk the West being wrecked by the economic consequences of a prolonged closure of Hormuz that would be entailed by their angry veto of Trump’s mooted ‘deal’? Possibly because Jewish ‘Big Money’ — since the 2008 crisis and the subsequent structural transfer of wealth from the real economy to the financialised ‘trader élite’ — may lead them to feel immune to economic downturn. They may even see it as an ‘opportunity’ (leading to assets going cheap).

The Iran effect, if not the direct cause, nonetheless marks a point of a significant reshuffling of global geo-politics. For, Israel it is bad news. The current Israel narrative is that no deal is better than a bad deal, because Israel could always return to war with Iran in a year or two’s time.

No one believes that, of course. Israel cannot mount war on Iran without full assistance from the US. And tomorrow’s America — in its relations with Israel — likely will be different from today’s.

Israeli commentator Nahum Barnea in Yediot Ahoronot has written,

“We [Israel] are sliding into a never-ending war on three, perhaps four fronts, holding territories that are not ours, with soldiers we do not have, in a bloody war against enemies we do not know how to deter — and all without giving real security to our citizens. Israel must break out of the Iranian trap. [Yet] Netanyahu is the last person who has the ability to extract us from it”.

Russia is changing too (partly under the effect of Iran). Strategic patience is over, and the recent deadly Ukrainian drone attack on a college dormitory in the Russian town of Starobelsk which killed at least 21 people, mainly teenage girls, was described Moscow as “the last straw”. The Russian public is justly furious.

Moscow holds European capitals and Kiev responsible for the recent Ukrainian barrage of drones and missiles fired deep into Russia, taking advantage of NATO airspace in the attempt to sidestep Russian air defences. Additionally, Russia has issued formal notification to Washington (via a telecon with Maro Rubio in India) that it holds European capitals and Kyiv responsible for the collapse of the Anchorage framework as well.

Russia has said that it intends to put an end to Ukraine’s ability to carry out further such attacks, and to liquidate the decision centres that plan and direct the attacks on Russians — even if it means killing US and European personnel. On 15 April, Russia’s Defence Ministry published lists containing the names and addresses of over 20 European companies and joint ventures allegedly supplying drones and components to Ukraine. Senior Russian officials, including Security Council Deputy Chairman Dmitry Medvedev, explicitly designated these international facilities as “potential targets” for Russia’s armed forces.

Europe has been warned.

Again, it seems that the Trump-Xi and the Putin-Xi summits in Beijing serve to mark the transition into a more hard-nosed geo-political era.

The two summits, one after the other, seem to have incentivised China into loosening its customary caution in order to put a brake on US attempts to widen dollar use, at the expense of the Yuan. The US Treasury’s ‘grand strategy’ is to ‘contain’ China’s current competitive advantage by raising its capital and energy costs. The US Treasury first tried imposing tariffs on China, but after failing with that ploy, turned to trying to squeeze China’s competitive advantage by blockading Chinese oil imports (naval blockades of Iran and Venezuela) to raise China’s energy costs.

However, if Trump wants all out trade competition, it seems to be ‘game on’ now for China — No more Mr (Xi) nice guy.

China is responding to Trump not with sanctions, nor with missiles. It is doing something far more precise: They are exerting counter pressures back at the US economy, and are doing this by cutting money flows into the dollar sphere in reaction to the US attempt to grossly widen global dollar use.

Both the US Genius and the Clarity Acts are contrived to suck out retail holders of local overseas currencies from their positions through inducing them to switch into crypto tokens denominated in dollars and backed by US Treasuries. If successful, this would both widen the US dollar reach and provide a new source of demand for US debt. Similarly (under the Clarity Act), investors looking to hold assets could be swapped out of regular US stocks and bonds into digital tokens, via a digitised distributed ledger system.

In short, the US aims to scoop up as much overseas currency as it can to insert into US markets via crypto — (effectively swapping the declining Petro-dollar for a substitute Crypto dollar hegemony that would then generate the dollar demand necessary to keep the US bond market from failing).

So, China is countering by going after something more sensitive — the flow of Chinese retail money going into American stocks and bonds. Chinese authorities have cracked down hard on Hong Kong brokerages that were helping Chinese mainland money flow into US markets. As matters stand, Wall Street depends on foreign buyers of stocks to a significant extent, but Chinese savings dwarf those of all other countries. These will no longer be available.

Secondly, China, the largest holder of gold in the world, will open a new gold trading centre in Hong Kong in July. This is a major move to break the western hold over precious metal trading — it strengthens the role of the Yuan and enables oil sales to be settled in gold (Saudi Arabia, in a roundabout way, is reportedly already selling oil to China via gold).

Thirdly, Euroclear, one of the world’s largest financial companies and the backbone of international settlements, is planning to accept Chinese bonds traded in Hong Kong — as ‘good collateral’.

Economist Sean Foo explains:

“When Euroclear accepts Chinese bonds as collateral, that means those bonds are treated as equivalent to liquid cash. It means they are good enough to back all international transactions – meaning that the global financial plumbing will be incorporating Chinese debt into the core infrastructure”.

“Now there’s a reason why Chinese bonds are becoming attractive to global investors, and this goes beyond just geopolitics or trade flows. It comes down to one fundamental reason. China is sitting on over $50 trillion in bank deposits. That’s more than the combined bank holdings of the EU, US and Japan. And that creates something every bond market, such as China’s needs in order to function well — a deep, reliable base of domestic buyers — your own local people buying”.

In sum, as more money flows into Chinese bonds, and the Yuan bond market deepens, Chinese borrowing costs stay low. So Beijing can fund itself cheaply and almost indefinitely — and thus can outlast the US grand strategy to contain China by squeezing both its capital costs and its energy costs.

https://conflictsforum.substack.com/p/iran-war-effect-marks-the-resetting