Sick Behavior From Financial Psychopaths

The Fed is likely thinking bailout or backstop for private credit, while banks look to monetize its demise.

I’ve been saying this for months: despite “experts” just sounding the alarm moments ago: the private credit unwind that started months ago and has now spiraled into a very real liability for the economy wasn’t some unknowable tail risk lurking in the shadows.

It couldn’t have been clearer if it was a fucking neon sign blinking THIS ENDS BADLY hanging outside of the 4 train station on Wall Street so industry workers were forced to see it on their way into work every morning.

Not only did I call the private credit collapse, I also argued that it would experience a sharp downturn before the Fed stepped in to bail it out or provide a backstop, despite, once again, the widespread misconduct of mismarking positions and carrying opaque, low-quality assets on the books of the companies managing these funds.

And here we are, right on schedule, watching that script unfold with all the subtlety of Eric Swalwell on a date after 9 whiskey cocktails.

In the last two days alone, Bloomberg reports that the Federal Reserve has gone from politely observing to actively interrogating. Not in a press-release, “we’re monitoring conditions” sort of way, but boots-on-the-ground examiners asking major banks to cough up details about their exposure to private credit.

Translation: they’re not trying to understand the industry, they’re trying to figure out how bad the damage could get and who’s going to be holding the bag when it does.

And what are they likely finding? Exactly what anyone paying attention already knew. Private credit funds didn’t just lend money, they borrowed it, too. Because in good times, leverage makes returns look smooth and irresistible. It turns middling loans into “high-yield opportunities.” It creates the illusion of stability. But in bad times? That same leverage becomes a transmission mechanism, turning localized stress into systemic risk. It’s not a bug, it’s the design.

Meanwhile, the Treasury is now poking around insurers, because of course this nuclear dogshit being peddled as a financial opportunity didn’t stay neatly contained in some alternative-assets sandbox. It likely spread. Into insurance portfolios, retirement products, retail funds…basically anywhere someone was desperate enough for yield to believe the pitch. The industry ballooned to roughly $1.8 trillion (and depending on how you count it, more), all built on the comforting fiction that because it wasn’t traditional banking, it somehow wasn’t subject to traditional banking problems.

Just like we’re seeing with “magically” successful subprime lenders like Carvana, of course they’re still subject to reality. The better question is how they can avoid the assumption they have to face reality at some point. I think we know how Carvana has been doing it: fucking with the numbers. And private credit is doing the same. Just with worse transparency.

And now suddenly regulators are “assessing spillover risk,” which is the bureaucratic equivalent of checking where the fire exits are while the building is already filling with smoke.

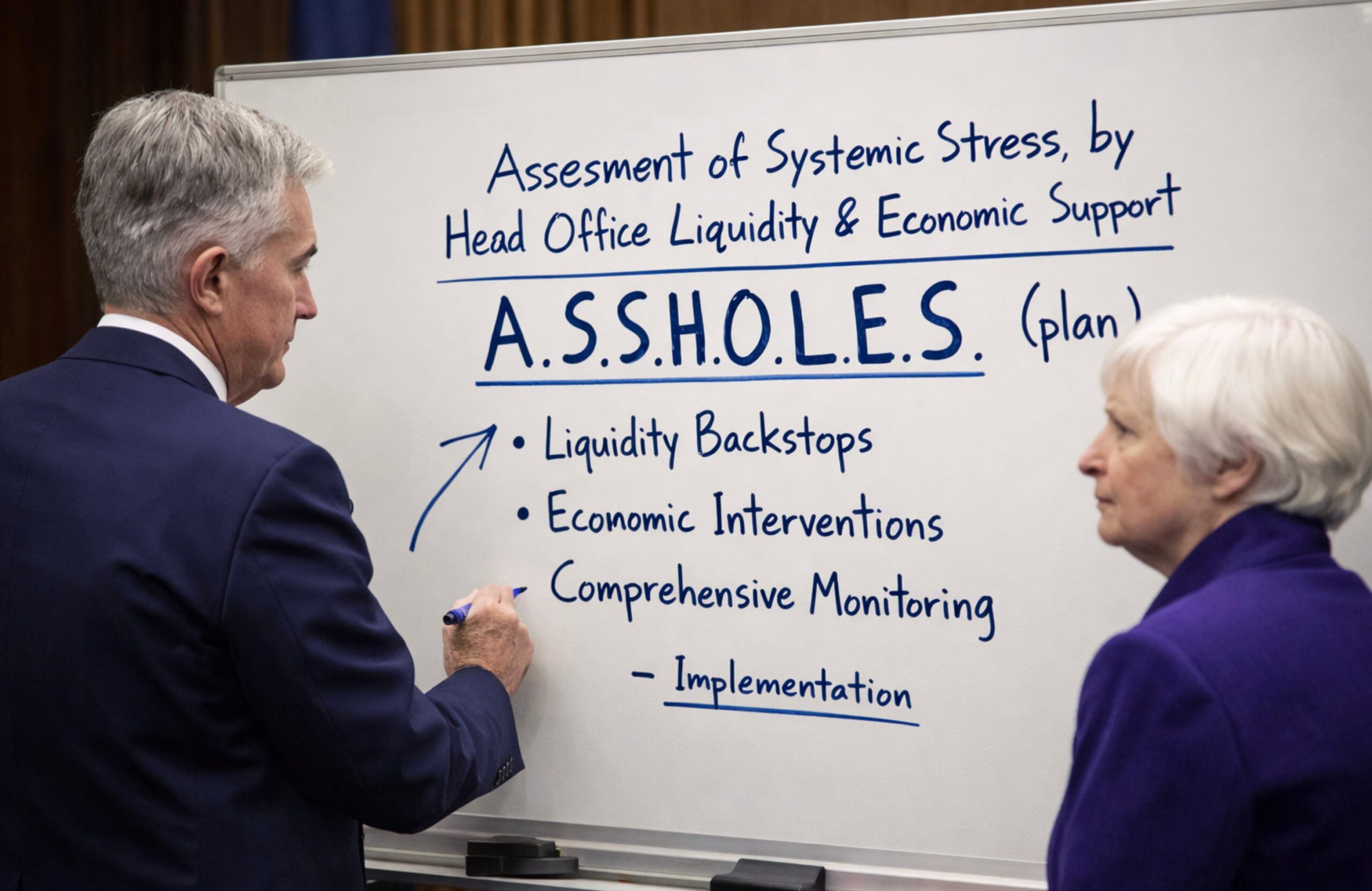

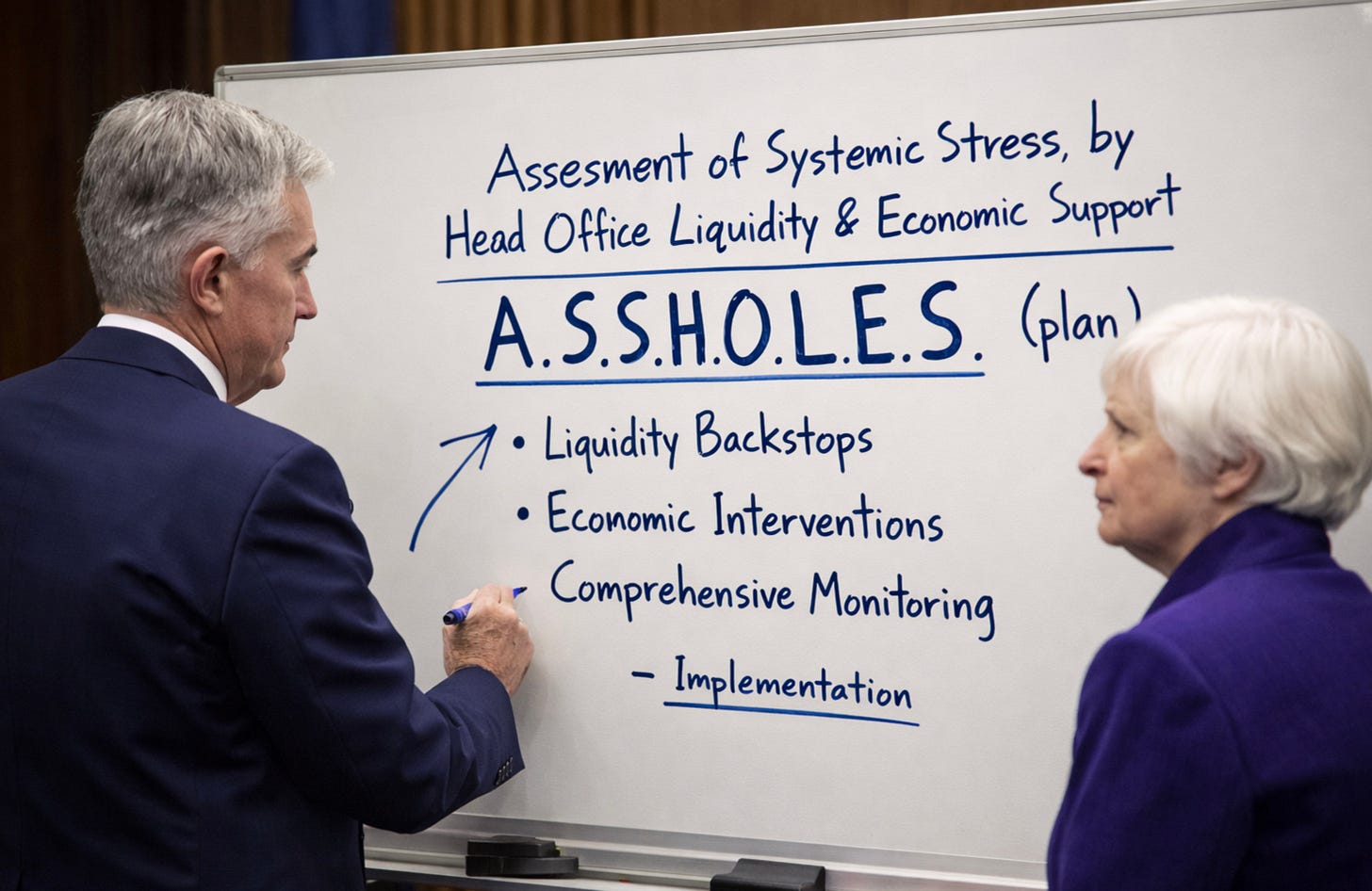

Let’s not pretend we don’t know where this goes. When the Fed starts mapping exposures like this, it’s not because they’re writing a research paper. It’s because they’re quietly preparing the intervention. Maybe it’s a backstop. Maybe it’s liquidity support. Maybe it’s some creatively named facility that sounds temporary but lingers for years (something like the “Assessment of Systemic Stress by Head Office Liquidity & Economic Support” plan, or A.S.S.H.O.L.E.S. for short).

Whatever form it takes, the direction is obvious: if this thing threatens the broader system, it will be contained and we will print our way out of it. Which is to say, the everyday worker, already suffering from inflation and unable to buy a box of Triscuits or a Domino’s Pizza, will now be responsible for bailing out private credit with their purchasing power.

And right on cue—this is where the story stops being predictable and starts being grotesque. Because while regulators are measuring the crater, Wall Street is building a gift shop next to it.

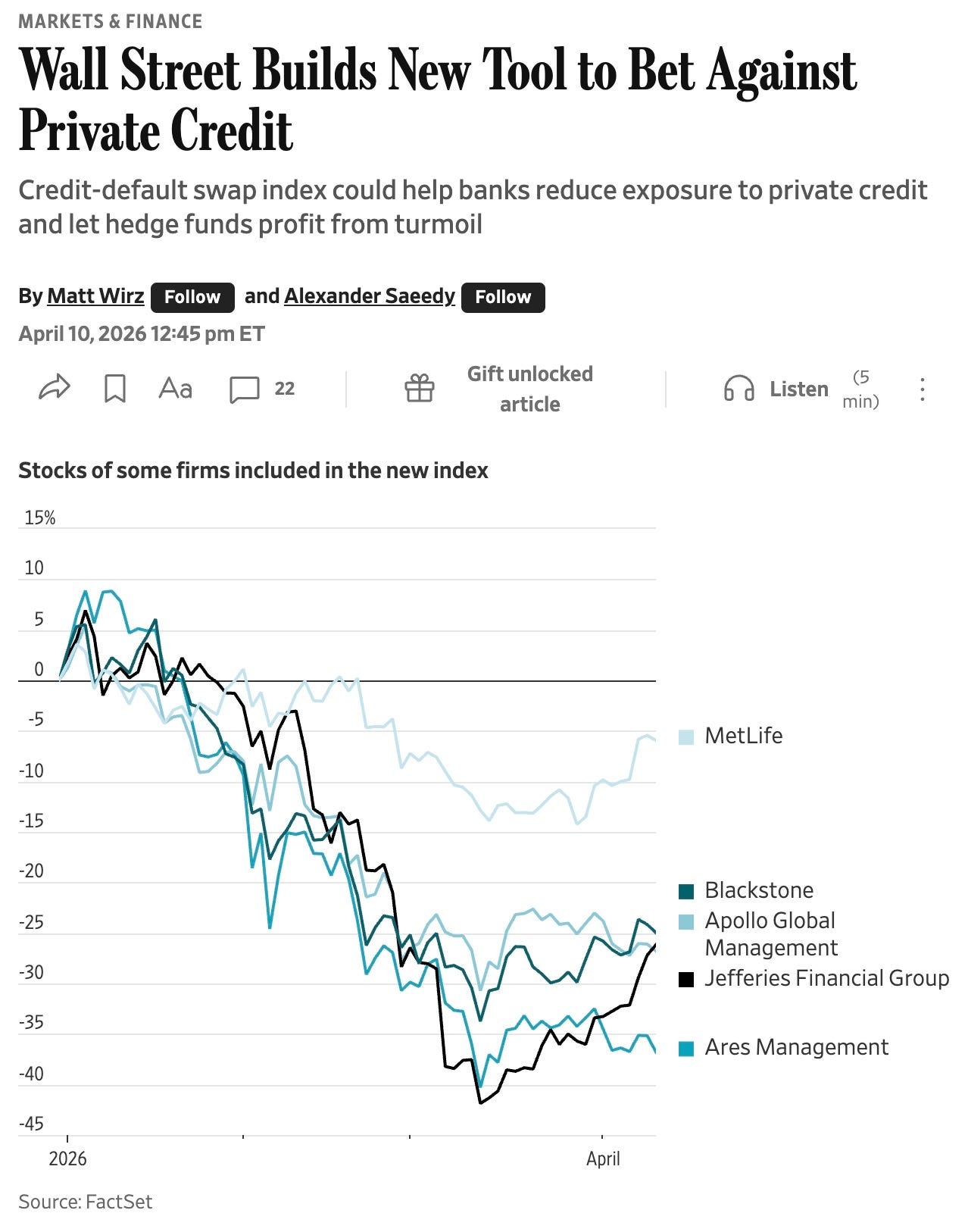

The Wall Street Journal wrote yesterday that banks like JPMorgan Chase, working with S&P Global, are rolling out a brand-new shiny instrument: a credit-default swap index tied to private credit exposure. A clean, tradable, scalable way to bet against the very ecosystem they spent the last decade inflating. They’re packaging up the risk, labeling it, and selling access to its failure.

You really have to admire the efficiency, right?

The index pulls in names like Apollo Global Management, Ares Management, and Blackstone, the giants of the space, the architects and beneficiaries of the private credit boom. As sentiment turns and defaults rise, the index goes up. In other words, the worse things get for the underlying system, the better things get for anyone positioned against it.

If this is giving you déjà vu, congratulations, you were alive in 2008.

Back then, the game was subprime mortgages. Banks originated garbage, distributed it widely, then quietly built instruments to short it when the cracks appeared. Today, it’s private credit wearing a slightly more sophisticated suit, but the choreography is identical. Manufacture the asset. Scale it. Normalize it. Then monetize its collapse from every conceivable angle.

And of course, the official justification is “risk management.” Banks say they need these tools to hedge exposure, to protect themselves from potential losses tied to private credit funds. Which, sure, fine. But let’s not insult anyone’s intelligence. This isn’t just about hedging. This is about creating a liquid, standardized market for betting on distress. It’s about turning systemic fragility into a profit center.

Hedge funds are already circling, because until now, shorting private credit was messy. You had to pick off individual securities, make indirect bets, deal with illiquidity. It was cumbersome. Inefficient. Now? They get a big, convenient index…a one-click way to express the view that the whole structure is wobbling.

So step back and look at the full picture, because it’s almost too on-the-nose to be real.

Wall Street spends years constructing a massive, opaque, leveraged lending machine and sells it as safe, stable income. It pulls in institutions, then pensions, then retail investors. always expanding the circle of exposure. Stress builds quietly, then not-so-quietly. Defaults tick up. Liquidity tightens. Investors panic. Douchebags in bowties warn about it after it is too late.

Regulators step in…not to dismantle the system that created the risk, but to understand how big the rescue might need to be. And at the exact same moment, the financial industry engineers new ways to bet against the collapse it set in motion.

This is moral hazard elevated to an art form. The downside is cushioned, implicitly or explicitly, by the expectation of intervention. The upside is captured privately, twice: once on the way up through fees and leverage, and again on the way down through shorts and derivatives. It’s not just asymmetric anymore, it’s circular. A closed loop of profit extracted from creation, expansion, and destruction alike.

And the most absurd part is how little effort is made to hide it. The Fed’s questions aren’t secret. The new derivatives aren’t backroom deals. This is all happening out in the open, narrated in real time by headlines that read like satire but aren’t.

And don’t be fooled. None of this bullshit is innovation. Not resilience. Not sophisticated risk transfer, or any other fancy sounding term they give it.

Nah. It’s just a deeply, structurally, almost impressively sick and psychotic ecosystem, where the same people who built the toxic dump of deals are now lining up to profit from its collapse, all while the adults in the room quietly prepare to make sure the fallout doesn’t inconvenience them too much.

And the everyman, honest hardworking plumber or mailman who can’t afford a box of cereal or a cup of coffee anymore because his purchasing power has been decimated by the same money printing that’ll inevitably be coming? Oh, well, fuck that guy. He has had his boot on the neck of Wall Street for just too damn long.

https://quoththeraven.substack.com/p/sick-behavior-from-financial-psychopaths