The CBDC We Already Have

Crypto on a chain.

The product was sold as the alternative.

Permissionless, censorship-resistant, beyond the reach of any single government.

The whole pitch of crypto, repeated in white papers and conference keynotes for fifteen years, was that this was the exit. The dollar system had become weaponised, the rails could be cut at will, but the chain – the chain was sovereign.

Iran took it as advertised. After getting kicked off SWIFT in 2012 and again in 2018, Tehran did exactly what every sanctions-evasion playbook recommended. Bitcoin mining legalised in 2019. Subsidised power rerouted to industrial farms.

Over $3 billion moved through digital assets in 2025 alone. The central bank held at least $507 million in USDT, the supposedly neutral dollar-substitute that wasn’t subject to any single government’s say-so.

As recent as April 22nd, Tron founder Justin Sun declared his blockchain “the most decentralised in the world”.

On April 23rd, the US Treasury called Tether and asked them to freeze $344 million of Iranian funds on Tron. Tether did it in one single smart-contract call. Two wallets, blacklisted at the issuer level, $213 million in one and $131 million in the other.

That money didn’t move or got seized. It instantly became decorative. Visible on the chain, but immobile, a monument to a successful misrepresentation.

Bessent named the campaign “Economic Fury”, which sounds like a 1990s wrestling pay-per-view but is apparently US Treasury policy now. The doctrine is straightforward: if we don’t like you, even your stablecoin is not yours anymore.

This is supposed to be SWIFT 2.0. Iran thought it was. And it delivered exactly as advertised. Just not as expected. SWIFT got weaponised in ‘12 against Iran and ‘22 against Russia; now the alternative has been weaponised the same way. Every sovereign actor on earth is currently re-reading the USDT terms of service and noticing some things they didn’t notice before.

Welcome to your CBDC.

About six months ago I wrote about why nobody actually wants a CBDC (link). Programmable money is restricted money, restricted money trades at a discount to unrestricted money, and any government trying to force a CBDC into circulation runs straight into Gresham’s Law. China’s been pushing the digital yuan for four years and it’s still only 0.16% of the money supply. People don’t want it. Even when state employees are paid in it, they cash out the second they can.

So how do you get programmable, permissioned, freezable digital money into circulation without anyone noticing it’s a CBDC?

You let someone else issue it. Then you regulate the issuer.

Last July, in what Washington genuinely branded “Crypto Week”, Congress executed the trick in plain sight. On July 17th, the House passed the Anti-CBDC Surveillance State Act 219 to 210, banning the Federal Reserve from issuing a programmable digital dollar. The bill’s sponsor warned on the House floor that a state-issued CBDC would be “an Orwellian surveillance tool” capable of freezing accounts and tracking every transaction.

Days later, the President signed the GENIUS Act, “Guiding and Establishing National Innovation for U.S. Stablecoins”, a name that took a committee of grown adults to produce. The Act requires every regulated stablecoin to be fully backed by short-term US Treasuries, with law enforcement integration baked into the compliance layer.

It looks like consumer protection. It technically is. It also is a CBDC with extra steps.

The Fed can’t issue a programmable, freezable, surveilled digital dollar. A private company in El Salvador can though.

Tether now holds $141 billion in US Treasury exposure. 17th largest holder of US government debt on the planet. More than Germany. More than the UAE. More than South Korea. A private company headquartered nominally in El Salvador owns more US Treasuries than most G20 nations. (link)

I’m hard-pressed to believe that’s a side effect.

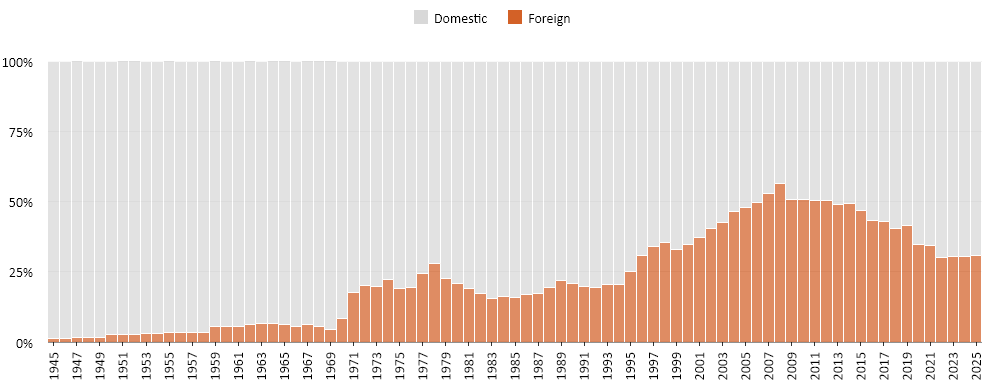

China dropped its UST holdings from $1.3 trillion to $683 billion. Japan’s been quietly selling. Foreign ownership of the Treasury market collapsed from 50% during the GFC to about 30% today. JPM estimates each $300 billion drop in foreign holdings pushes yields up roughly 33 basis points. With $9.2 trillion rolling over in 2025 and another wave queued for 2026, the Treasury needs new buyers. Badly. Like, “we just regulated a $200 billion private company into being one” badly.

So they engineered one.

Stablecoin issuers, by law, must hold short-term Treasuries. The market is projected to hit $2 trillion by 2028, meaning roughly $1.5 trillion in Treasury demand, materialised out of crypto liquidity. Beautiful. Clean. Foreign capital that wouldn’t touch a UST directly walks in through the stablecoin side door, holds USDT, has no idea it’s holding the same paper with extra steps.

And it is was working.

Now nine months later, the Treasury froze $344 million on a Thursday afternoon.

Nine months. That’s the gap between signing the GENIUS Act and demonstrating to every sovereign on earth that USDT is freezable on demand. The first cycle of this pattern, SWIFT becoming a strategic asset and then a sanctions weapon, took about thirty years. The dollar reserve system, eighty. Western gold custody, considerably longer. Each iteration runs faster than the last.

You can almost hear the Saudi sovereign wealth fund switchboard lighting up.

Because the lesson of 2022 was that dollar reserves are confiscatable when the political winds shift (link). The world watched $300 billion of Russian central bank reserves vanish from the asset column overnight, and central banks have been buying gold ever since. Over 1,000 tonnes a year, three years running. Poland, Turkey, India, China, Hungary – all stacking. Not because gold is sexy. Because gold doesn’t take phone calls from Washington.

Now the US has demonstrated the same lesson on the rails it just spent two years building. Stablecoin reserves can be frozen at the issuer layer; the GENIUS Act codified it, the Iran freeze made it visible. Every sovereign treasurer on earth now knows that holding USDT is functionally identical to holding US Treasuries with an extra “freezable on demand” feature bolted on top. Which is to say: worse than holding Treasuries. Same exposure, strictly more political risk.

I’m sure that’s fine.

The pattern is hard to miss at this point. SWIFT was sold as neutral plumbing. They weaponised it anyway. Dollar reserves were sold as the global safe asset. They froze Russian reserves anyway. Western custody of foreign gold was sold as inviolable. They blocked Venezuelan repatriation anyway (link). And now stablecoins were sold as the workaround, the alternative built specifically to recover the foreign demand the previous weaponisations destroyed – and they’ve been used the same way before the cement on the GENIUS Act has dried.

Each instrument gets weaponised. Each weaponisation destroys the demand the instrument was built to attract. Each new instrument has to recover the trust the last weaponisation destroyed.

Lucy will keep moving the football because Lucy can’t help it. The interesting question is who’s still showing up to kick.

Sovereigns probably won’t. They’ll be shunning USDT the same way they’re shunning Treasuries – but quietly, steadily, they’ll be accounting for its political risk. Some might rotate into BTC, but the precedent has been set. A crypto is only as sovereign as long as the code allows.

What I think that USDT will become from here on out is a small-transactional CBDC. Retail users everywhere. Think Western Union in seconds with less fees. But the sovereigns who want a hedge that actually works? They’ll be stacking gold.

The most telling detail in the whole story isn’t even the freeze. It’s what Tether does with its own profits.

The company made $10 billion in 2025. It holds $141 billion in Treasuries because regulation says it has to. But it also holds $17.4 billion in physical gold and $8.4 billion in Bitcoin, funded out of excess profits and accumulated at a rate of two tons of physical gold per week. Their CEO stood on a stage in San Salvador in front of a slideshow of literal storm clouds and predicted the end of the dollar system.

Tether is the largest non-sovereign buyer of US Treasuries on earth and is hedging against the collapse of the United States.

Yup. I’m sure it’s fine.

The architecture would have been a beautiful solution to a real problem. Stablecoins move money in seconds worldwide, all the while absorbing Treasury supply, and foreign demand walks right back in, capital that normally doesn’t trust Washington still ends up funding it. The trust deficit gets papered over with code.

It could have worked.

They didn’t even bother waiting a year to abuse the budding trust.