Tulip Bulbs in Geostationary Orbit — the Insanity of Space X’s $1.7 Trillion Valuation

Boy, do we have inflation! And we’re not referring merely to yesterday’s +4.2% Y/Y gain on the CPI and today’s +6.5% Y/Y rise in the PPI.

The ultimate inflationary eruption, in fact, is coming squarely at us in tomorrow’s absurd $1.7 trillion IPO of Space X. After all, the relentless central bank monetary inflation of the last several decades did not mainly end up on main street, and it most surely did not disappear silently into the equivalent of a financial black hole.

To the contrary, it flooded into Wall Street and the linked and related asset markets all around the planet, sending valuations soaring into the financial stratosphere.

And we do mean biblical flood of fiat credit. When the Greenspan era got rolling in 1990, the combined balance sheets of the Big Six central banks (Fed, ECB, BOJ, PBOC, BOE and Swiss central bank) totaled $2.0 trillion and represented just 14% of the GDP of their consistence economies.

But after the print-a-thons of the dotcom boom, the Great Financial Crisis of 2008-2009 and the pandemic era eruption of central bank bond-buying, the combined footings of the Big Six central banks stood at $32 trillion and 68% of their constituent GDP by 2022.

To put those gargantuan numbers in perspective, just consider where these balance sheets would have stood by 2022 under Professor Milton Friedman’s 3.0% annual growth of the money supply, based on the correct idea of zero inflation and long-run potential GDP grwoth of about 3.0% per year.

The answer would have been the $2.0 trillion starting point of 1990 would have grown to $5.0 trillion by 2022. So the Big Six central banks along probably generated upwards of $27 trillion of excess central bank credit even under Friedman pro-central bank economic model. And needless to say, that massive excess of cheap, high-powered money ended up in the great financial bubbles of the present era.

As it happens, we have no particular beef against Elon Musk, and believe he has been one of the great capitalist entrepreneurs of the present era—-to say noting of his charitable endeavors, such as rescuing X from the Deep Staters and attempting to shed some DOGE-light on the massive waste in the Federal budget.

But where we do take issue is with the cult following that his business ventures have attained in the Fed-fueled, bubble-ridden financial markets. In the case of Tesla, there is nothing special about his vehicles in a congested, over-supplied EV market that has now slowed down to 5-7% annual growth compared to one-time surges of 20% to 35% a few years ago.

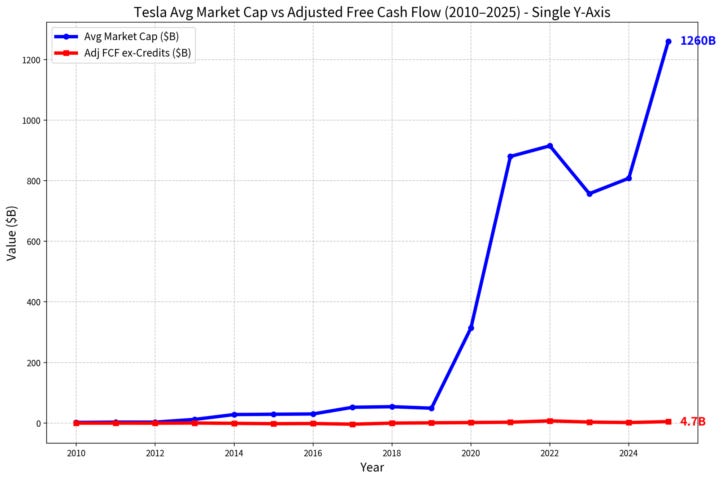

As it happens, however, notwithstanding slumping growth and aggressive competition, ranging from the giant auto industries of China and Japan to the formidable luxury European automakers, Tesla is still trading at this very moment at 305X adjusted free cash flow!

That’s right. Its current market cap of $1.26 trillion dwarfs it adjusted free cash flow into a rounding error. And, to be clear, we are not talking about Tesla’s sales multiple or its so-called PE multiple based on Wall Street’s hideously bloated measures of “adjusted” EPS.

Instead, we are talking about the only thing that creates enterprise value and market cap over time: That is, cash flow after all business expenses, interest payments, cash taxes and CapEx have been deducted.

The graph below, obviously, leaves nothing to the imagination. The Tesla cult in the Wall Street casino has driven its market cap (blue line) skyward, from barely $100 billion in 2019 to $1.260 trillion at present—even as its free cash flow has barely inched along the floorboards of the graph.

If there were ever an example of bottled air speculation, surely it is indicated by the graph below. Tesla valuation is just plain insane because its not actually even based on its free cash flow.

Instead, it stems from an out-of-this-world driver-less vehicle narrative that may or may not come to pass. But if it does it will surely see the entire existing auto industry jumping into the frey by making and leasing vast fleets of driver-less vehicles under existing brands or countless new ones to yet be invented.

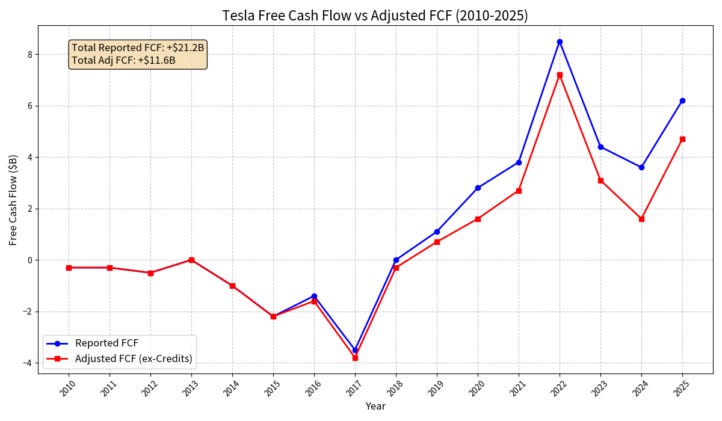

Moreover, there is a reason we have based the red line on “adjusted” free cash flow, and that’s because even the meager amounts of cash from operations after CapEx that Tesla has reported over the years were materially flattered by goverment mandated EV credits from its competitors.

Alas, those credits didn’t create value—they simply stole it from the competition at government gunpoint.

Accordingly, since it went public in 2010, Tesla has generated a scant $21.2 billion of reported free cash flow. Yet upwards of $10 billion of that didn’t have anything to do with making cars, and everything to do with lobbying governments for the helping hand of EV credits.

But now that every automakers has jumped into the EV game, those credits are going the way of the do-do bird in any event.

Needless to say, the only way you can possibly explain the impending $1.7 trillion IPO of Space X is that Wall Street is attempting to merge the Tesla cultists with the AI fanatics into a financial mania that has not been witnessed since the Dutch Tulip Bulb Mania of 1635.

That is to say, if you think the above Tesla nosebleed valuation is crazy—trading at 305X its honest (adjusted) free cash flow while burning through capital like a drunk sailor on shore leave— then buckle up. You ain’t seen nothing yet.

Elon Musk’s latest financial Frankenstein, the newly public Space Exploration Technologies Corp. (soon to trade as SPCX), is gunning for a $1.7 trillion market capitalization on the back of an S-1 that reads like a science fiction prospectus crossed with a venture capitalist’s fever dream. Thus—

- No indication of sustainable free cash flow? Check.

- Massive losses masked by narrative? Double check.

- A “hidden AI plan” that supposedly justifies Elon’s sojourns to Mars? That too!

This is not investment analysis. This is financial insanity enabled by the longest period of monetary distortion in modern history. As we indicated above, central banks printed trillions, crushed yields to zero (and below), and created a world where discounted cash flows from 2040 look more real than actual earnings today.

SpaceX — rebranded and stuffed with things formerly known as xAI, X, and orbital fantasies — is the ultimate expression of this delusion. So it behooves us to tear open the S-1 filed May 20, 2026, and see what the numbers actually say—even as the hopium merchants rewrite reality with reckless abandon.

The S-1 Numbers: A Cash Furnace Disguised as a Space Empire

Consolidated revenue actually tell a story of decelerating momentum. SpaceX reported respectable sales jumps from $10.4 billion in 2023, to $14.0 billion in 2024 and $18.674 billion in 2025. Yet Q1 2026 came in at just $4.694 billion, which annualizes to a 2026E run-rate of roughly $18.8 billion — essentially flat with 2025.

Thus, the three-year CAGR from 2023 to this 2026E run-rate is only about 22% per annum. That’s respectable for a private rocket company, but it is not remotely near the triple-digit sales growth rates the valuation implies.

Here are the consolidated and segment figures straight from the filing:

- Revenue: 2025 $18.674 billion (2026E run-rate ~$18.8 B)

- Adjusted EBITDA: $6.58 billion in 2025.

- GAAP operating loss: –$2.589 billion in 2025;

- Q1 2026 operating loss: -$1.943

- 2025 Capex: $20.7 billion (more than full-year revenue).

- Implied 2025 free cash flow: -$14.1 billion

- Q1 2026 investing outflows:-$16.0 billion.

At the segment level, the figures for 2025 show no signs of what used to be called profits and free cash flow:

- Connectivity Segment (primarily Starlink), which is the only real cash engine

- Revenue: $11.387B (61% of total; up 50% YoY)

- Operating Income: $4.423B

- Adjusted EBITDA: $7.168B (63% margin)

- Segment FCF: roughly $3B+ in 2025.

- This segment is carrying the entire company.

- Space (launch services, NASA contracts, Starship development)

- Revenue: $4.086B (22% of total; up only ~8% YoY)

- Operating Loss: -$657M

- Adjusted EBITDA: $653M

- Capex/R&D drag: ~$3B in Starship alone

- Segment FCF: Deeply Negative

- AI (xAI + related compute/X platform)

- Revenue: $3.201B

- Operating Loss: –$6.355B

- Adjusted EBITDA: $-1.237B

- Capex: $12.727B (61% of total company capex)

- Segment FCF: Catastrophically negative — the black hole devouring Starlink profits.

The pattern is unmistakable: Starlink generates real cash. Everything else is a capital incinerator.

Consolidated free cash flow remains deeply negative because the $20.7B+ capex (mostly AI and Starship) swamps the operating cash flow from the connectivity engine.

At a $1.7 trillion valuation on a $18.8 billion revenue run-rate, SpaceX IPO is being priced at roughly 90x sales and over 250x Adjusted EBITDA — with actual free cash flow still deeply negative.

There is no rational DCF model on Earth that gets you to $1.7 trillion without assuming growth rates that would embarrass even the most aggressive 1999 dot-com analyst.

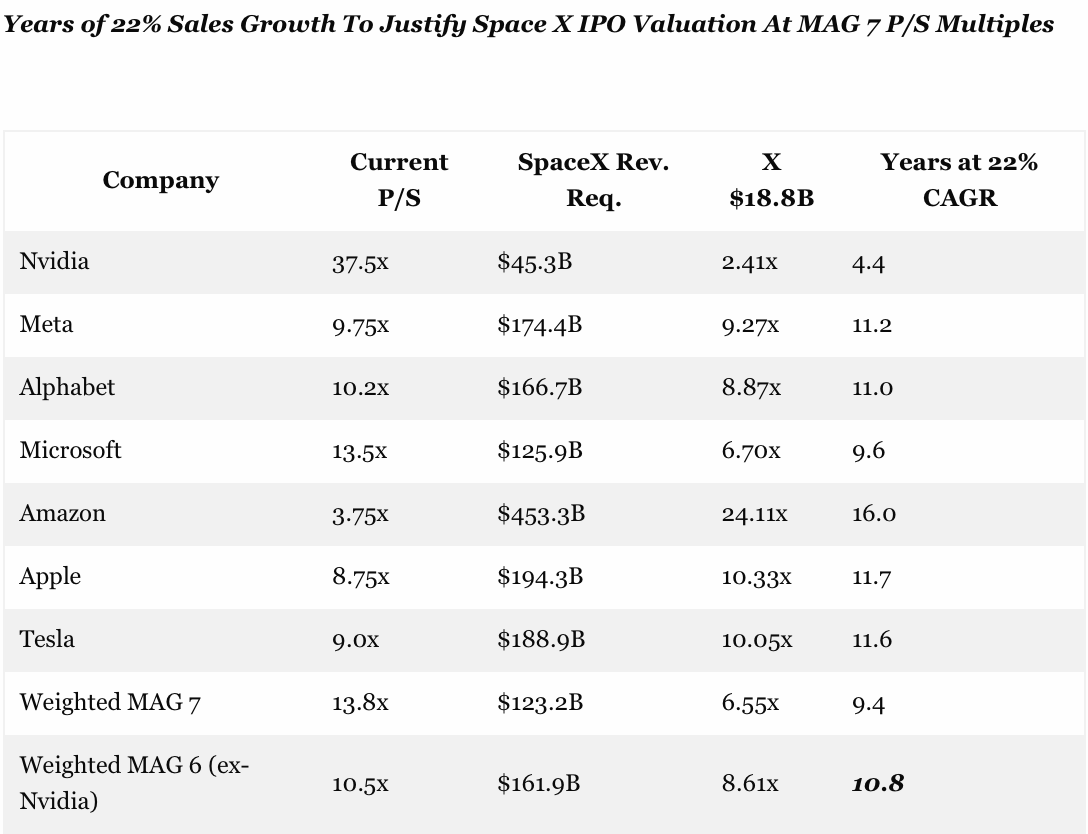

In order to put this valuation insanity in proper perspective, we have calculated what it would take for SpaceX to “grow into” a $1.7 trillion market cap using the current super-high sales multiples from the Magnificent 7 tech giants.

The table shows:

- The current market cap to sales multiple for each of the Mag 7 (P/S).

- The SpaceX revenue that would be required at that multiple to foot to $1.7 trillion of market cap.

- The ratio of this required revenue to Space X’s LTM sales.

- The years needed to justify the P/S multiple for each Mag 7 comparable at Space X’s current 22% per annum sales growth rate (even though that has slowed sharply in the past year)

So take Alphabet (Google) as the prime example. GOOG currently trades at approximately 10.2xtrailing sales. For SpaceX to be worth $1.7 trillion at that same multiple, it would need $166.7 billionin annual revenue — nearly 9 times its current run-rate.

At a sustained 22% CAGR, that would take 11 years of flawless execution with no dilution.Even using the more reasonable Weighted MAG 6 (excluding the Nvidia outlier) of 10.5x, SpaceX would still need $161.9 billion in revenue — requiring roughly 10.8 years at 22% growth.

These are extraordinarily optimistic assumptions, to put it mildly. In the real world, growth rates slow dramatically as the revenue base expands. Dilution from massive ongoing capex is inevitable. And mature companies rarely trade at the same premium multiples they enjoyed in their hyper-growth phase.

So the valuation math here is not merely aggressive: it is totally delusional.

At the Heart of This Crazy Valuation: Elon’s New Version of “Pie-in-the-Sky” — “Data Centers in the Sky”

At the heart of this crazy valuation is Elon Musk’s newest version of “pie-in-the-sky,” which might be called “data centers in the sky.” That is, we need to forget the fantastical junkets to Mars of Space X’s days gone by. Instead, the Wall Street underwriters have pivoted hard to the narrative that the real prize is orbital AI infrastructure.

Starship, we are told, will become the ultimate GPU shuttle, delivering cheap, high-cadence launches of massive compute constellations. In space you supposedly get free solar power, vacuum cooling, and no earthly grid constraints.

Musk talks of gigawatt-scale clusters and eventually terawatts. Analysts nod along, projecting AI revenue exploding from $3.2 billion today to hundreds of billions by 2030.

Yet and yet.This doesn’t cut the mustard. Not even close. The list of “known unknowns” surrounding orbiting data center operation and maintenance is staggering.

First, radiation. Low-Earth orbit and beyond expose electronics to constant cosmic rays and solar particle events. Terrestrial data centers already spend heavily on error-correcting code and redundant systems. In space, you would need extreme radiation hardening — far beyond what current GPU clusters use — dramatically raising costs and reducing performance. A single major solar storm could wipe out entire constellations.

Second, thermal management. Vacuum is a terrible heat sink. On Earth, we use air, water, and massive cooling towers. In orbit, you need exotic radiators, heat pipes, and active systems that add weight, complexity, and failure points. Heat rejection in space is a notorious engineering nightmare for large-scale compute.

Third, latency and connectivity. Most AI training and inference still needs low-latency interaction with Earth-based users, data sources, and other clusters. Round-trip latency from orbit is orders of magnitude worse than terrestrial fiber. Synchronizing distributed orbital compute with ground systems introduces massive complexity and inefficiency.

Fourth, maintenance and upgrades. On Earth, you walk into a data center and swap a failed server in minutes. In orbit, a failed node means either accepting permanent loss or launching expensive repair missions. Starship may eventually lower launch costs, but rendezvous, docking, and robotic servicing at scale remain science fiction for the foreseeable future. The idea of regularly upgrading millions of GPUs in orbit is pure fantasy.

Fifth, power reliability. While solar arrays sound attractive, they must contend with orbital night cycles, degradation from radiation and micrometeorites, and enormous array sizes needed for gigawatt-scale clusters. Battery storage in space adds further mass and risk.

Sixth, regulatory and geopolitical risk. Who regulates orbital data centers? What happens if a major power (China, Russia) decides to interfere? Space debris, collision risks, and international treaties add layers of uncertainty that no terrestrial hyperscaler faces.

Seventh, capital intensity and economics. Even if technically feasible, the upfront capex to orbit, assemble, and power these systems would be astronomical — likely dwarfing anything Starlink has required. The S-1 already shows AI capex devouring $12–16 billion per quarter. Scaling that to orbital reality would require hundreds of billions more, with returns delayed by years or decades.

These are not speculative “unknown unknowns.” These are well-understood engineering and economic barriers that have caused previous space-based compute concepts to die quiet deaths. Yet the narrative soldiers on because it sounds futuristic and justifies today’s nosebleed valuation.

The Analyst Fairy Tales Continue.

Wall Street’s finest aren’t even pretending anymore. The pitch deck and S-1 TAM (total addressable market) disclosures lean hard into this orbital AI dream. Goldman Sachs reportedly modeled AI revenue exploding from $3.2 billion to $322 billion by 2030 — a 100x ramp that anchors the entire $1.75 trillion valuation.

This is classic Musk Cult narrative layering. SpaceX was supposed to be about reusable rockets and Mars. Then Starlink became the savior. Now it’s data centers in the sky.

Each pivot justifies ever-higher valuations while the core profitable business (Starlink) subsidizes massive losses elsewhere.

The S-1 itself admits Starship is the single biggest execution risk. Delays there crater the entire thesis.

Guidance? What Guidance?

The S-1 is deliberately light on formal numerical guidance. Informal signals point to aggressive ramps, but no concrete, auditable three-to-five-year forecasts. The market is being asked to trust the vision: losses today are “investments.” The dilution and debt are temporary. Orbital AI is the prize.

This is the same song Tesla bulls sang for years. SpaceX now faces the same risks, amplified by even greater capital intensity and technical complexity.

The Bigger Picture: Printing Press Money’s Final Act

SpaceX at $1.7 trillion with negative free cash flow and $20+ billion annual capex is not a sign of strength. It is the terminal symptom of a monetary regime that destroyed price discovery. When real yields were negative and liquidity infinite, of course, any story with “exponential” and “disruptive” in the pitch deck could fetch trillions.

Now, with QT ongoing and inflation scares rising, the margin for error is shrinking by the week. Investors buying at these levels are not investing in rockets or satellites. They are buying Elon’s vision at a 90x+ sales multiple, betting he can execute multiple moonshots simultaneously while competitors, physics, regulators, and capital markets always and everywhere cooperate. Fully. Perfectly.

History says otherwise. Previous manias — railroads, radio, dot-com stocks, clean-tech booms — delivered real technologies but destroyed enormous paper wealth in the process. Most high-flyers became footnotes or shadows of their peak valuations.

So SpaceX will likely survive and deliver genuine advances in launch and connectivity. Starlink is a real business with strong economics. But a $1.7 trillion valuation assumes perfection across unproven domains — including the fantastical “data centers in the sky” — while ignoring the cash furnace burning today.

The Weighted MAG 6 analysis shows it would still require more than a decade of perfect execution just to grow into a reasonable multiple — and even then “reasonable” on the basis of the super-high multiples carried by the Mag 7 bubble today.

The broader economic context makes this even more perilous. Global debt loads are unsustainable. Governments have over-promised on green and tech transitions they cannot afford. When the next recession hits — and one is always coming — speculative growth names get hit hardest.

An old and proven Law Of Markets applies here: Bubbles driven by easy money and government-enabled narrative always overshoot on the way up and crash harder on the way down.

Tesla has been the poster child. SpaceX is now auditioning for the same role on an even grander stage.

If Tesla at 305X FCF was crazy, SpaceX at these levels is clinically insane. The S-1 lays it bare for anyone willing to read past the glossy TAM slides. The rest is hopium, narrative, and the eternal greater-fool trade.

Drive (or launch) carefully. The bubble’s countdown has begun.

https://davidstockman.substack.com/p/tulip-bulbs-in-geostationary-orbitthe