Will Evicting Blackstone Help Young People Buy Homes?

Mega investors are a mega problem. But not the only one.

It’s hard to get consensus in Washington, but nearly everyone agrees there’s an epic housing crisis. Mega institutional investors, many in both parties agree, need a mega purge.

President Donald Trump has taken a rhetorical hatchet to the Blackstones and Vanguards for snapping up starter homes, saying that “another pillar of the American dream that has been under attack is homeownership” during his State of the Union address, and that “we want homes for people, not for corporations. Corporations are doing just fine.”

The idea of limiting their access to the housing market has bipartisan support. The 21st Century ROAD to Housing Act cleared the Senate in a 89-to-10 vote Thursday and is now with the House, which passed its own housing bill in February. It would ban companies that own 350 or more homes from buying more, responding to lobbying from the White House and an executive order Trump signed to that effect.

But the problems with the housing market are many, and the details have gotten relatively little attention in the press.

“No one gives a s— about housing,” Trump reportedly told House Speaker Mike Johnson last week as he seeks to clinch the SAVE America Act, an election security bill that has more momentum, according to Punchbowl News.

The argument goes like this: Big firms buy single-family homes and squeeze out people attempting to climb onto the first rung on the homeownership ladder. They cannibalize the modern version of the company town, minus the store, with a ruthlessness that would give Henry Potter a gleam in his eye.

“Typically people’s first home … is the stock they’re [institutional landlords] going to buy,” said Stephen Billings, a real estate professor at the University of Colorado. “So it is cutting off that first home-buyer channel.”

But these investors are one problem among many, including supply shortages, inflation, and interest rates. Starter homes number roughly 550,000, making up just 1 percent of all housing, according to economist Thomas Malone of Cotality.

The problem of the housing food chain remains. It may be insurmountable.

At the bottom are the lower-cost, entry-level homes: a three-bedroom, two-bath, 1,600-square-foot house, for example. In a healthy market, those buyers build equity, then sell and move up the chain. That starter home becomes available for the next household. The middle of the chain is your typical “move-up” home: a four bedroom, three bath, 2,500 square feet house, for growing families that have also increased their income. If people in the move-up homes never upgrade, it gums up the whole chain.

Meanwhile, institutional investors have been increasing their presence in Washington in an effort to contain any damage.

The National Home Rental Council spent $327,500 to lobby Congress and the White House in 2025, according to OpenSecrets.org.

The Housing Food Chain

The U.S. housing market depends on mobility — people moving up, freeing up space behind them. That’s not happening.

It’s been well-documented that institutional investor landlords swept in like vultures during the Great Recession to purchase homes that were in or on the verge of going into foreclosure.

Blackstone was one of the early investors, paying more than $1 billion in 2012 to gobble up 6,500 foreclosed houses. Similar investment firms like Vanguard followed. Companies like American Homes 4 Rent, Invitation Homes, and Home Partners of America soon became common in many neighborhoods, particularly in the South.

Then came COVID-19 in 2020. The Federal Reserve’s extraordinary monetary response, most importantly its purchases of $2.8 trillion in mortgage-backed securities, brought rates to around 3 precent for conventional mortgages (Freddie Mac and Fannie Mae) and 2.5 percent for Federal Housing Administration and Veterans Affairs mortgages (Ginnie Mae).

These historically low rates allowed millions of existing borrowers to refinance at rock-bottom levels, while also giving homebuyers access to cheap financing. The combination of fiscal and monetary stimulus policy was too much. By mid-2022, we had runaway inflation. Mortgage rates soared to 8 percent in 2023.

A lock-in on housing occurred. Suddenly, many people couldn’t afford to sell. They would be giving up a 3 percent mortgage in exchange for a 7 percent rate. The difference in monthly payments between the two on a 30-year mortgage is an eye-popping 58 percent.

Cold Hard Cash

Homes are actually relatively affordable for the median American according to a commonly used index, but in some markets, especially where institutional buyers have a heavy presence, affordability isn’t the only problem.

The National Association of Realtors publishes a widely-followed Housing Affordability Index, which compares the nation’s median income to the income needed to qualify for a mortgage on a median-priced home. The break-even line is 100, meaning the median-income household has exactly enough income to qualify. The higher the number, the better for housing affordability. Anything below 100 means the median-income household falls short.

The index hit a record low of 92.2 in 2023 and, despite a modest rebound as rates cooled, the current 109.1 rate remains well under the historical average since 1986 of 136.95.

But Billups says institutional investors offer other advantages to sellers, including cold hard cash.

“There’s not uncertainty about mortgage approval, they give you cash, it’s quicker closing, they don’t ask for a bunch of repairs,” he said. “They typically just take it as is. And so a lot of sellers prefer that and are willing to even take a discount on the sales price to get there.”

Malone agrees.

Institutional investors are “probably more likely to be waiving any inspection contingencies because their risk is diversified out amongst many thousands of properties.” And when it turns into a bidding war, he adds, “they’ve got deeper pockets than the individual buyer. They can just outbid you.”

Crowding On The Lowest Rung

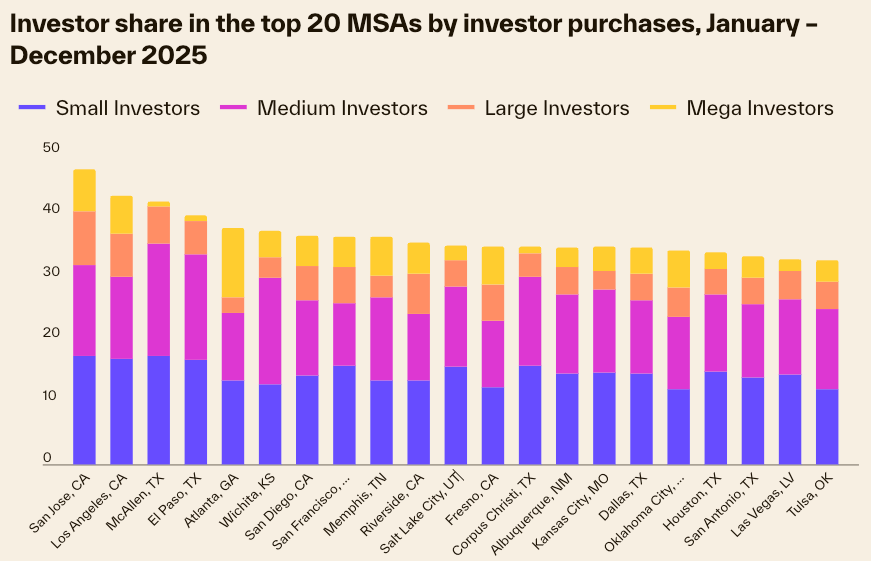

Nationally, the biggest institutional owners are a small slice of a huge market, but they are not evenly distributed through the different price tiers.

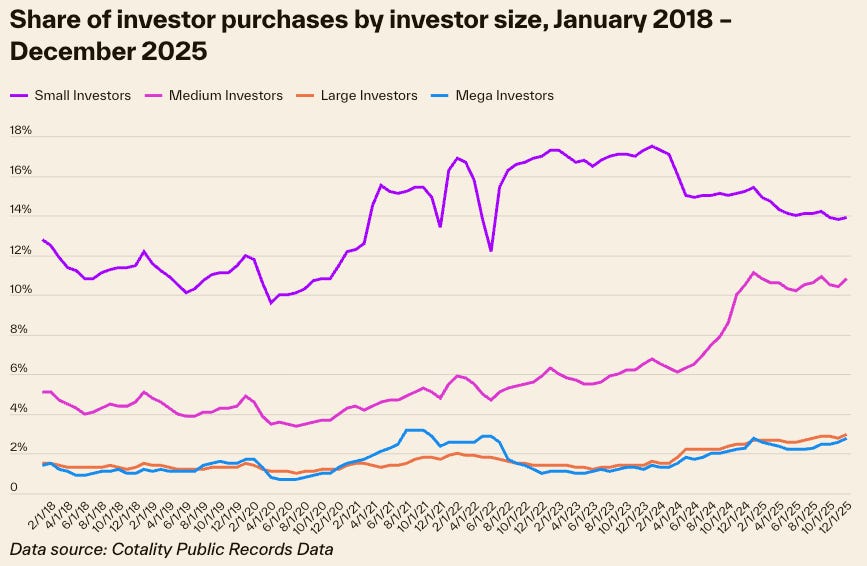

While investors made up 30 percent of nationwide home purchases in 2025, according to Cotality’s data, large investors (more than 100 homes) and mega investors (more than 1,000) represent just 3 to 6 percent of all housing sales since 2018.

But large investors concentrate in precisely the starter-home rung that a first-time buyer is trying to get on.

“So generally they have a higher market share in lower price single-family homes,” Malone said. “Those are the people on the margin of renting and buying. So that’s where most of the rental demand is.”

If you’re a buyer hoping to grab the 1,600-square-foot starter home, it doesn’t matter that institutional investors don’t own the whole market. They’re bidding on your rung of the ladder.

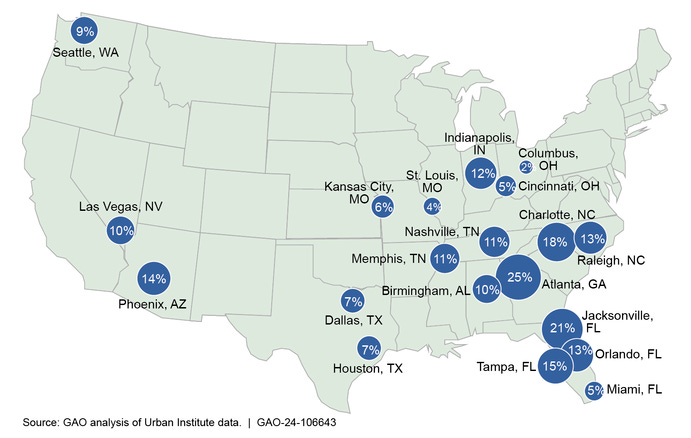

Institutional investors are also not evenly distributed across the country. In Atlanta, mega investors comprise a whopping 11.1 percent of home purchases.

“Atlanta sticks out as an outlier,” said Malone.

Other markets where institutional investors dominate single-family rental housing stock include Atlanta (25 percent); Jacksonville, Fla. (21 percent); Charlotte, NC (18 percent); and Tampa (15 percent).

Bidding Against A Computer

Institutional investors can work faster too. Jordan Ash of the Private Equity Stakeholder Project points to comments made in 2021 by the then-CEO of institutional investor Progress Residential, Chaz Mueller.

“…we get an automatic feed every 15 minutes for every home in our buy box across our markets. So when a home goes on the market, within 15 minutes we get a feed if it meets our criteria. We have an algorithm that quickly scores it and helps does the underwriting…We have an acquisition team that has a couple of inputs. They put in the rents and the renovation budget and they try to generally get an offer out within a couple of hours of the home going on the market. So we’re able to analyze it very quickly, make an offer. Our offers are all cash, very flexible closing. Basically whenever the seller wants to move out, we’re happy with that.”

At the time, Muller said Progress had a portfolio of about 45,000 homes. The private company has since grown to about 94,000 homes in more than 30 markets, according to its 2024 impact report.

“You just kind of can’t compete with that,” Ash said, adding that this jeopardizes the biggest source of wealth for many families.

“To the degree that they sell them, they sell them to each other,” Ash said.

Build-to-Rent

Jessica Moreno of the group Action NC, who has gone door-to-door over the last few years to organize people for a tenants union, noted institutional investors are increasingly moving to building houses for the purpose of leasing them.

“Because it’s more profitable. You make your own homeowners association, you set the prices for the entire neighborhood… that’s where the market is going,” she said.

Billups, the University of Colorado researcher, found that neighborhoods in the Charlotte area with a high concentration of institutional owners had a relative decrease in property values of 1 to 2 percent.

“There are costs and benefits” of institutional investors, “but [build-to-rent] has an additional benefit of increasing supply,” Billups said. “I’d say stuff that increases supply, we should definitely not be restricting.”

The Senate bill requires that institutional investors with 350 or more properties sell the new properties they build after seven years, rattling the National Association of Home Builders, which called the provision “alarming.”

The Mortgage Bankers Association has also come out against the bill.

“We’ve been investing heavily into our government affairs efforts for years,” American Homes 4 Rent CEO Bryan Smith reminded investors on Feb. 20. “Active engagement allows us to be at the center of a lot of these discussions and really get our message across that we are a key part of the housing solution.”

In other words, institutional investors wont be evicted without a fight.

https://www.racket.news/p/will-evicting-blackstone-help-young